In earnout M&A, the structures most likely to pay the seller are based on revenue milestones, last 12 to 24 months, include precise accounting definitions, and allow the seller to retain meaningful operational control after closing. The structures most likely to fail rely on EBITDA that the buyer controls, vague performance targets, long earnout periods, or unrestricted post-closing business changes. The difference is rarely the purchase price. It is almost always the structure.

Key Takeaways

- Revenue-based earnouts generally create fewer disputes than EBITDA-based earnouts.

- Earnouts lasting more than two years become significantly harder to achieve.

- Sellers should avoid performance targets they no longer control after closing.

- Every financial metric should be defined in the acquisition agreement before signing.

- Protective provisions such as acceleration clauses and limits on operational changes can determine whether an earnout is ever paid.

What an Earnout Actually Is

An earnout M&A provision is a form of contingent consideration, meaning that part of the purchase price is paid after closing only if agreed performance targets are achieved. Instead of paying the entire purchase price on day one, the buyer defers a portion of the consideration until the business reaches predefined milestones.

Most earnouts exist because the buyer and seller value the business differently.

The seller believes future growth justifies a higher valuation. The buyer agrees that the opportunity exists but wants evidence before paying the full amount. An earnout bridges that valuation gap by tying part of the purchase price to future performance.

If you are negotiating this type of transaction, the valuation process matters just as much as the earnout itself. A realistic valuation establishes whether an earnout is genuinely needed or simply being used to bridge an unrealistic pricing expectation. Learn more about Horizon M&A Advisors’ Business Valuation Services

On paper, this sounds reasonable.

In practice, an earnout changes the nature of the transaction. The seller receives less cash at closing and accepts future payment that depends on events occurring after ownership has transferred.

That distinction matters.

Once the buyer owns the company, they typically control hiring decisions, budgets, pricing strategy, marketing spend, capital investments, and accounting policies. Every one of those decisions can influence whether an earnout is achieved.

This is why experienced advisors spend far less time debating whether an earnout should exist and far more time examining how it is structured.

Advisor Insight

The headline purchase price often receives the most attention during negotiations. In reality, the structure determines the value. A $15 million offer with a poorly designed $3 million earnout may be worth less than a $13.5 million offer paid entirely at closing.

Why Earnouts Fail

Most failed earnouts in M&A do not fail because the business underperforms.

They fail because the seller loses control over the factors that determine whether the earnout will be paid.

After reviewing dozens of lower middle market transactions, a clear pattern emerges. The disputes rarely begin with dishonest intentions. They begin with incentives that changed the moment ownership changed.

The Earnout Stress Test

Before agreeing to any M&A earn out structure, ask five questions:

- Who controls the performance metric after closing?

- Can the accounting calculation change?

- Can the buyer materially change operations?

- Is the earnout period longer than necessary?

- Would an independent third party calculate the payment the same way?

If any answer creates uncertainty, the earnout deserves another round of negotiation.

The Buyer Changes the Business

This is the single most common reason earnouts fail.

The buyer acquires the business with every intention of integrating it into a larger organization.

Within months they may:

- Merge departments

- Replace senior management

- Change pricing strategy

- Reallocate sales territories

- Reduce marketing budgets

- Consolidate facilities

- Introduce new software platforms

None of these decisions are inherently unreasonable.

Many are exactly what buyers should do after an acquisition.

The problem arises when the seller is still measured against targets established before those operational changes occurred.

The seller remains accountable for results while the buyer controls the decisions that produce those results.

That imbalance creates disputes.

EBITDA Can Become a Moving Target

Revenue usually tells a straightforward story.

EBITDA often does not.

An EBITDA earnout can change dramatically after closing because buyers may legitimately allocate costs that never existed when the business operated independently.

Examples include:

- Corporate overhead

- Executive compensation

- Shared accounting teams

- Human resources expenses

- Enterprise software costs

- Integration consulting fees

- Information technology allocations

Every allocation reduces reported EBITDA.

The seller argues those costs are unrelated to the acquired business.

The buyer argues they are legitimate operating expenses.

Both positions can be reasonable.

Unfortunately, the earnout calculation now depends on accounting interpretation rather than business performance.

This is one reason sophisticated buyers perform extensive financial reviews before closing. Understanding what buyers examine during Due Diligence Services helps sellers identify potential areas of disagreement before they become expensive disputes:

Industry Perspective

Studies of private M&A transactions have consistently shown that post-closing purchase price adjustments and accounting disputes remain among the most negotiated provisions in acquisition agreements. The complexity increases when deferred consideration depends on financial metrics that either party can interpret differently.

Sellers Lose Control of the Target

One question reveals whether an earnout is fair.

Can the seller still influence the outcome after closing?

If the answer is no, the seller is accepting performance risk without retaining operational authority.

For example:

A seller agrees to an earnout based on customer retention.

After closing, the buyer replaces the customer success team.

Several key accounts leave.

The seller misses the earnout.

The metric was reasonable.

The control was not.

Whenever performance targets depend on pricing decisions, staffing levels, capital investment, production schedules, or sales strategy, sellers should identify exactly who controls those decisions during the earnout period.

If it is the buyer, the risk profile changes immediately.

Vague Definitions Create Expensive Problems

One of the shortest sentences in an acquisition agreement often causes the longest disputes.

“Earnout will be based on Adjusted EBITDA.”

Adjusted according to which accounting policy?

Which expenses are excluded?

How are extraordinary costs treated?

Are integration expenses included?

Can accounting policies change after closing?

If those questions are unanswered before signing, they will almost certainly be argued after closing.

Every undefined financial term becomes an opportunity for conflicting interpretations.

Long Earnout Periods Increase Uncertainty

Time is one of the most underestimated risks in earn out structure M&A agreements.

A twelve-month earnout measures execution.

A thirty-six-month earnout measures execution, economic conditions, competitive changes, leadership turnover, customer behavior, and industry cycles.

The longer the earnout period, the more variables neither party can control.

That does not automatically make long earnouts unfair.

It simply means the probability of disagreement increases every year.

Advisor’s Rule

If a buyer needs three or four years to determine whether your business performs as promised, ask whether the uncertainty comes from the business or from the structure itself. In many lower middle market transactions, a shorter and better-defined earnout produces a fairer outcome for both parties.

Structures That Actually Get Paid

Not every earnout M&A agreement is destined to end in a dispute.

In fact, some earnouts work exactly as both parties intended. The difference is that they are built around metrics the seller can influence, definitions both parties understand, and protections that anticipate what happens after closing.

After working on lower middle market transactions, I have found that successful earnouts usually share the same characteristics. They are simple enough that both parties know exactly how the payment will be calculated before the business changes hands.

The strongest earn out models for mergers and acquisitions are rarely the most complicated.

They are the easiest to explain.

If two experienced advisors cannot independently calculate the same earnout payment using the agreement, the structure is probably too complicated.

Revenue Milestones Usually Produce Better Outcomes

If I represent a seller, I generally prefer revenue-based earnouts whenever they accurately reflect the business.

Revenue is not perfect.

A buyer can still influence pricing, marketing investment, or customer strategy.

However, revenue is considerably more transparent than EBITDA because it depends less on accounting judgments made after closing.

An EBITDA earnout may be reduced by decisions such as:

- Corporate cost allocations

- Shared executive salaries

- Information technology expenses

- Integration projects

- Changes to accounting policies

Revenue does not eliminate disagreements, but it reduces the number of variables that can unexpectedly change after closing.

That is why many experienced advisors consider revenue milestones a safer starting point for earnouts in M&A, particularly when the buyer intends to integrate the acquired business quickly.

Advisor Insight

Every additional accounting adjustment creates another opportunity for disagreement. The fewer adjustments required to calculate the earnout, the more likely both parties will reach the same answer.

Shorter Earnout Periods Reduce Risk

Time creates uncertainty.

Every additional year introduces factors that neither buyer nor seller can fully predict.

These include:

- Economic slowdowns

- Industry disruptions

- Competitive pressure

- Leadership changes

- Customer concentration issues

- Supply chain interruptions

A twelve-month earnout primarily measures business execution.

A thirty-six-month earnout measures the economy, management decisions, market conditions, and strategic priorities that may have nothing to do with the business the seller originally built.

In most lower middle market transactions, I believe twelve to eighteen months provides enough time to validate performance without exposing both parties to unnecessary uncertainty.

Sellers Should Retain Meaningful Operational Control

One question determines whether an earnout is balanced.

Who controls the performance target?

If the seller remains responsible for achieving revenue or profitability goals, they should retain authority over the decisions that influence those goals.

That does not mean the buyer gives up ownership.

It means the acquisition agreement clearly defines which decisions remain with the seller during the earnout period.

Examples include:

- Sales pricing

- Hiring and terminating key employees

- Marketing budgets

- Customer relationships

- Capital expenditure approvals

- Product strategy

Without operational authority, the seller is effectively guaranteeing performance while someone else controls the business.

That is a position I generally advise clients to avoid.

Every Financial Definition Should Be Written Before Closing

Many earnout disputes begin with a phrase that appears harmless during negotiations.

“Payment will be based on Adjusted EBITDA.”

That language is incomplete.

A stronger agreement defines:

- Revenue recognition policies

- EBITDA calculation methodology

- Extraordinary items

- One-time expenses

- Corporate overhead allocations

- Accounting standards

- Financial reporting schedule

- Review and dispute procedures

Every definition agreed before closing removes one potential disagreement after closing.

The objective is simple.

The earnout should be calculated by mathematics, not negotiation.

Include Catch-Up and Acceleration Provisions

Well-designed earn out mergers and acquisitions agreements anticipate unexpected events instead of hoping they never occur.

Some of the most valuable protections include:

Catch-Up Provision

Suppose quarterly targets are missed because one large customer delays an order.

The customer signs during the following quarter, allowing the business to exceed the annual target.

Without a catch-up provision, the seller permanently loses part of the earnout.

With one, annual performance determines payment rather than temporary timing differences.

Acceleration Clause

If the buyer sells the acquired business before the earnout period ends, the seller should not lose the opportunity to receive deferred consideration.

Many experienced advisors negotiate provisions that require the remaining earnout to become immediately payable or calculated using predefined assumptions if another transaction occurs.

Operational Protection

The acquisition agreement should address questions such as:

- Can the buyer discontinue a major product line?

- Can they significantly reduce marketing investment?

- Can they merge operations with another division?

- Can they transfer employees supporting the acquired business?

If those actions directly influence the earnout calculation, they should also trigger protective provisions.

Use the Earnout Control Test

One framework I frequently use during negotiations is what I call the Earnout Control Test.

Before signing, ask these five questions.

| Question | Good Answer | Warning Sign |

| Who controls the performance metric? | Seller has meaningful authority | Buyer has complete control |

| Can accounting policies change? | Changes require mutual agreement | Buyer decides unilaterally |

| Is the target measurable? | Objective and easily verified | Subjective or open to interpretation |

| How long does the earnout last? | 12 to 24 months | More than 24 months |

| What happens if the buyer changes the business? | Agreement provides seller protections | No contractual safeguards |

If three or more answers fall into the warning column, I consider the earnout high risk regardless of the headline purchase price.

Decision Matrix: Which Earnout Structure Fits the Deal?

Different businesses require different approaches.

The table below illustrates how I typically think about earn out structure M&A decisions.

| Situation | Structure I Would Prefer |

| Business has predictable recurring revenue | Revenue-based earnout |

| Buyer plans immediate integration | Higher cash at closing instead of EBITDA earnout |

| Seller will remain CEO during transition | Revenue or EBITDA may work if definitions are tightly drafted |

| Business depends on a few large customers | Customer retention milestone with clearly defined rules |

| Financial reporting is inconsistent | Resolve reporting issues before accepting any earnout |

| More than 40 percent of the purchase price depends on the earnout | Renegotiate the consideration mix before signing |

Advisor’s Checklist

Before accepting an earnout, confirm that you can answer yes to each question:

- Do I still influence the performance metric after closing?

- Are all accounting definitions documented?

- Is the earnout period no longer than necessary?

- Does the agreement limit operational changes that could affect payment?

- Is there a catch-up or acceleration provision?

- Would an independent CPA calculate the payment exactly the same way as both parties?

If any answer is “no,” the discussion is not finished. Those issues are often worth more than negotiating another half turn on the valuation multiple.

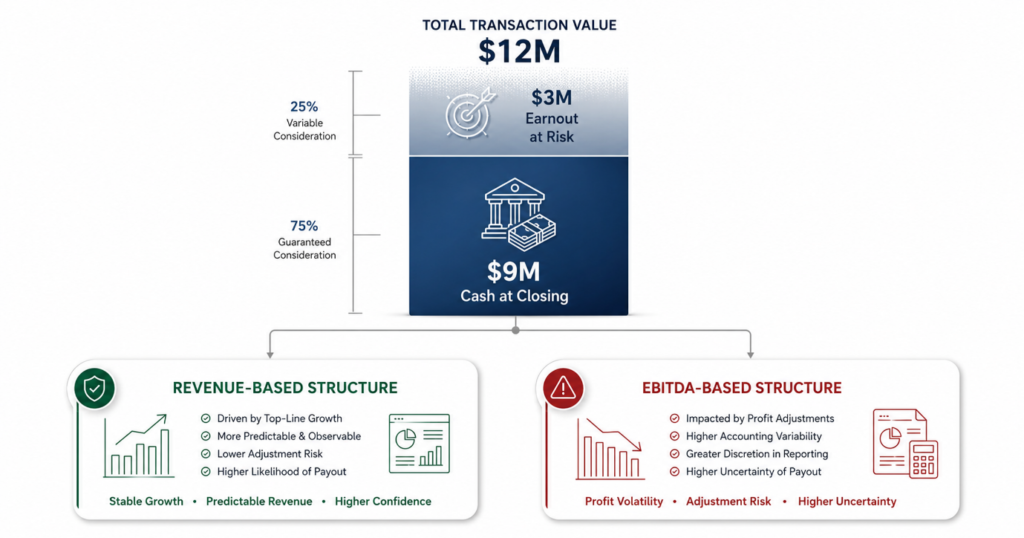

How One Earnout Structure Paid $3 Million While Another Paid NothingThe following example is illustrative and is intended to demonstrate how earnout structures affect seller outcomes. It is not based on a specific Horizon M&A transaction.

A privately owned manufacturing company receives an offer with a total purchase price of $12 million.

The buyer proposes the following deal structure:

- Cash at closing: $9 million

- Contingent consideration (earnout): $3 million

- Earnout period: 18 months

The seller is comfortable with the overall valuation because the business has consistently grown over the previous five years.

The discussion quickly shifts from “How much is the company worth?” to “Under what conditions will the remaining $3 million actually be paid?”

That is where many negotiations begin to change.

Scenario One: Revenue-Based Earnout

The parties agree that the seller will remain President during the earnout period.

The agreement specifies:

- Revenue target: $16 million

- Earnout period: 18 months

- Revenue recognition follows the company’s historical accounting policies.

- Material changes to pricing strategy require mutual approval.

- The buyer cannot materially reduce the sales team without written consent.

- Annual measurement includes a catch-up provision.

During the next eighteen months:

- Two large customers expand their contracts.

- One customer delays a purchase order by six weeks.

- Annual revenue reaches $16.4 million.

The seller receives the full $3 million earnout.

Neither side argues about accounting.

Neither side hires litigation counsel.

The metric was objective.

The responsibilities were clear.

The agreement anticipated normal business fluctuations.

The earnout worked exactly as intended.

Scenario Two: EBITDA-Based Earnout

Now change only one part of the agreement.

Everything else remains identical.

Instead of measuring revenue, the earnout is based on EBITDA.

Six months after closing, the buyer begins integrating the acquired company into its existing platform.

The buyer:

- Allocates corporate accounting expenses.

- Charges executive management salaries to the acquired business.

- Implements a new ERP system.

- Increases cybersecurity spending.

- Moves procurement into a centralized purchasing department.

None of these decisions violate the acquisition agreement.

In fact, many buyers would consider them responsible integration activities.

Revenue still exceeds expectations.

Customers remain satisfied.

Sales continue growing.

However, reported EBITDA falls below the earnout threshold because of newly allocated operating costs.

The seller receives:

$0

Nothing about the underlying business changed.

Only the accounting inputs changed.

That single structural decision determined the outcome.

Advisor Insight

When two earnouts have the same headline value but one depends on accounting judgments after closing, they are not economically equivalent. The structure determines the certainty of payment.

The Advisor’s Take: How I Would Negotiate an Earnout

Every seller eventually asks the same question.

“What should I fight for?”

My answer surprises many owners.

Do not spend most of your negotiation arguing over the headline purchase price.

Spend it negotiating the rules that determine whether deferred consideration will ever be paid.

I have seen sellers negotiate another $500,000 in theoretical purchase price while overlooking language that ultimately decided whether they received millions of dollars in earnout payments.

The mechanics deserve at least as much attention as the valuation.

What I Would Fight For

If I represented a seller, these would be my highest priorities.

Objective performance metrics

The easier the metric is to verify, the fewer disputes arise later.

Whenever possible, I prefer metrics that require minimal accounting interpretation.

Short earnout periods

Every additional year introduces more uncertainty than value.

Most lower middle market businesses can demonstrate performance within twelve to twenty-four months.

Detailed accounting definitions

Never rely on broad phrases such as “Adjusted EBITDA.”

Every adjustment should be documented before closing.

Operational protections

If the seller remains responsible for achieving performance targets, the agreement should clearly define which operational decisions remain under the seller’s authority.

Regular reporting requirements

Do not wait until the earnout expires to discover how performance is being measured.

Monthly or quarterly reporting allows both parties to identify disagreements early.

Acceleration provisions

If the buyer sells the business before the earnout period ends, deferred consideration should not simply disappear.

The agreement should specify exactly how remaining payments will be handled.

What I Would Be Willing to Concede

Not every negotiation point deserves equal attention.

I am generally comfortable discussing:

- Quarterly versus annual measurements

- Staged earnout payments

- Reasonable performance adjustments supported by historical trends

- Payment timing after measurement periods

These issues usually affect cash flow rather than the likelihood of payment itself.

When I Would Recommend Walking Away

Sometimes the smartest negotiation strategy is refusing the structure entirely.

I become cautious when:

- More than 40 percent of the purchase price depends on the earnout.

- The buyer has unrestricted authority to change operations.

- EBITDA definitions remain vague.

- The earnout period exceeds three years.

- The seller has little or no influence over the performance target.

A larger headline valuation does not always create a better deal.

Guaranteed cash at closing often has greater value than contingent consideration that depends on variables outside the seller’s control.

This is where experienced Business Sale Advisory becomes particularly valuable. Many successful negotiations focus less on increasing the purchase price and more on improving the quality of the deal structure itself.

Earnout vs. Seller Financing

Business owners often compare earnouts with seller financing because both defer part of the purchase price.

The two structures create very different risks.

| Earnout | Seller Financing |

| Payment depends on future business performance. | Payment follows a predetermined repayment schedule. |

| Seller assumes operational and performance risk. | Seller primarily assumes buyer credit risk. |

| Payment amount may change. | Payment amount is generally fixed. |

| Frequently involves accounting interpretation. | Usually governed by loan terms. |

| Greater potential for post-closing disputes. | Greater focus on repayment security. |

Neither structure is automatically superior.

The better choice depends on why the buyer is proposing deferred consideration.

If the buyer genuinely believes future growth justifies a higher valuation, an earnout may make sense.

If the objective is simply to bridge a financing gap, seller financing may provide greater certainty.

The important point is understanding which risk you are accepting before signing.

Seller’s Earnout Review Checklist

Before signing your Letter of Intent, confirm the following:

✓ The performance metric is objective.

✓ You still influence the outcome after closing.

✓ Accounting definitions are fully documented.

✓ Operational changes are appropriately restricted.

✓ Reporting requirements are clearly defined.

✓ Catch-up and acceleration provisions are included.

✓ An independent CPA would calculate the payment exactly the same way.

If any of these items remain unresolved, the earnout deserves another round of negotiation before you sign.

Frequently Asked Questions

What is an earnout in M&A?

An earnout is a form of contingent consideration where part of the purchase price is paid after closing if agreed performance targets are achieved. It allows buyers and sellers to bridge valuation differences while sharing future performance risk.

How are earnout payments calculated?

Earnout payments are typically based on predefined revenue milestones, EBITDA milestones, customer retention targets, or other measurable business objectives. The acquisition agreement should specify the calculation methodology, accounting standards, reporting schedule, and payment timeline.

Why do earnouts fail?

Most earnouts in M&A fail because sellers lose control after closing while remaining responsible for achieving performance targets. Buyer operational changes, new cost allocations, vague accounting definitions, and overly long earnout periods are among the most common causes of disputes.

Can a buyer avoid paying an earnout?

A buyer cannot simply refuse to pay an earnout that has been properly earned under the acquisition agreement. However, if the agreement gives the buyer broad discretion over accounting policies or operational decisions, legitimate business actions may reduce the reported performance below the required threshold. This is why careful drafting is essential.

How long should an earnout period last?

Most experienced advisors prefer earnout periods between twelve and twenty-four months. Longer periods expose both parties to greater market uncertainty, operational changes, and integration risks, increasing the likelihood of disagreement.

What happens if the buyer changes the business after closing?

Unless the acquisition agreement includes protective provisions, buyers generally have the right to operate the business as they believe appropriate. Sellers should negotiate limitations on material operational changes, reporting requirements, and acceleration clauses before signing to reduce the risk of unexpected outcomes.

Final Thoughts

An earnout is not inherently good or bad.

It is simply a tool.

When the performance metric is objective, the seller retains meaningful influence over the business, and the acquisition agreement clearly defines how payments are calculated, an earnout can bridge a valuation gap and help both parties complete a transaction that might not otherwise happen.

When the metric depends on accounting judgments, the buyer has unrestricted control over operations, or the agreement leaves important terms open to interpretation, the earnout can become the most disputed part of the deal.

The question every seller should ask is not:

“How much is the earnout worth?”

The better question is:

“What has to happen for me to actually receive it?”

That shift in thinking often changes the entire negotiation.

Before signing any Letter of Intent or Purchase Agreement, evaluate the earnout with the same level of scrutiny you would apply to the purchase price itself. A well-structured earnout should create alignment between buyer and seller, not uncertainty about whether deferred consideration will ever be paid.

If you are evaluating an offer that includes an earnout, the experienced advisors at Horizon M&A Advisors can help you assess the structure, identify hidden risks, and negotiate terms that protect your financial outcome.