A net working capital peg is the agreed target level of normalized operating working capital that a business is expected to deliver at closing. It is typically based on the trailing 12-month average of normalized working capital, adjusted for seasonality, growth trends, and one-time items. The closing working capital is then compared against this target, and any shortfall or excess results in a purchase price adjustment through the closing statement or post-closing true-up.

Why the Net Working Capital Peg Matters

Most sellers spend months negotiating valuation, deal structure, and tax implications. Surprisingly, many pay far less attention to the working capital peg, even though it can reduce their proceeds by hundreds of thousands of dollars without changing the agreed valuation multiple.

The reason is straightforward. Most middle-market acquisitions are completed on a cash-free, debt-free basis. Buyers expect the business to be transferred with enough operating working capital to continue running normally on day one.

If the business delivers less than the agreed net working capital target, the buyer is effectively funding the operating shortfall after closing. The purchase agreement usually protects the buyer by reducing the purchase price dollar for dollar.

For example, imagine a business sells for an enterprise value of $12 million. The valuation does not change. However, if the closing balance sheet shows working capital that is $350,000 below the agreed peg, the seller’s proceeds are typically reduced by the same amount.

This surprises many owners because they assume negotiations are finished once the purchase price is agreed. In reality, the final amount they receive often depends on the working capital calculation completed immediately before or shortly after closing.

In some transactions, the adjustment happens before funds are released. In others, it becomes part of a working capital true-up, where the final closing balance sheet is prepared after the transaction closes. Either way, the financial outcome is identical. A lower working capital position results in less cash reaching the seller.

This is one reason experienced buyers devote significant attention to working capital due diligence. Small accounting decisions made during diligence can materially affect what ultimately lands in the seller’s bank account.

Likewise, sellers often focus on maximizing valuation while overlooking the mechanics that determine what they actually keep. Understanding how the peg works is just as important as understanding valuation itself, especially because both directly influence the final proceeds from the transaction. Learn more about how valuation and deal structure interact through professional business valuation services.

How the Net Working Capital Peg Is Actually Calculated

Despite the negotiation that often surrounds it, the calculation itself is relatively straightforward.

The challenge lies in deciding which numbers belong in the calculation and which should be removed.

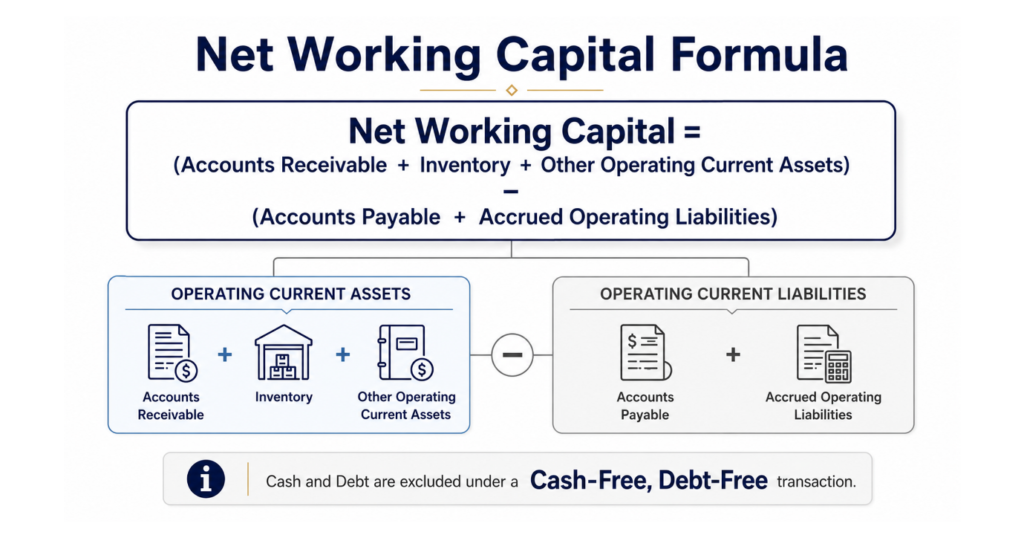

The starting point is net working capital, calculated using only operating current assets and operating current liabilities.

Formula

Cash, debt, shareholder loans, income tax balances, and other financing-related accounts are normally excluded because the transaction is negotiated on a cash-free, debt-free basis.

Once monthly operating working capital has been calculated, the buyer and seller typically review the historical balance over the previous twelve months.

For businesses with stable operations, a trailing 12-month average is often sufficient.

For businesses with significant seasonality, the review period frequently extends to 18 or even 24 months.

A landscaping company, HVAC contractor, agricultural supplier, or holiday product manufacturer may experience substantial fluctuations throughout the year. Using only the most recent few months could produce a peg that reflects temporary seasonal conditions rather than the business’s normal operating requirements.

Instead, advisors generally look for the level of working capital required to support the business throughout a complete operating cycle.

Normalization Matters More Than the Average

Many sellers assume the calculation is simply an average of historical balances.

In practice, the more important discussion is whether the historical numbers actually represent normal operations.

Suppose the seller deliberately delayed supplier payments during the month before closing. Accounts payable increases temporarily, making net working capital appear lower.

Most buyers will argue this is not representative of ordinary business activity and should not influence the peg.

The same applies when inventory has been intentionally reduced to generate additional cash before closing. Although this may improve short-term cash flow, it often leaves the buyer with insufficient inventory to operate normally after the acquisition.

Experienced financial advisors therefore prepare a schedule of normalized working capital before negotiations begin.

Typical normalization adjustments include:

- One-time prepaid expenses that will not recur after closing.

- Temporary spikes in accrued liabilities caused by unusual events.

- Customer deposits that relate to non-operating activities.

- Insurance recoveries or litigation settlements.

- Non-recurring tax-related balances.

- Timing differences created by year-end accounting adjustments.

The objective is not to produce the lowest possible peg or the highest possible peg.

The objective is to establish the amount of operating working capital that an independent buyer would reasonably expect the business to transfer on the closing date.

Growth Can Shift the Target

Historical averages are only part of the analysis.

A business growing at 30 percent annually often requires more receivables, more inventory, and additional operating capital than it did twelve months earlier.

Buyers frequently argue that historical averages understate future operating needs.

Sellers, on the other hand, may argue that future growth should not require them to leave additional capital inside the business at closing.

Both positions have merit.

This is why sophisticated negotiations rarely rely on averages alone. Advisors evaluate revenue trends, inventory turnover, receivable collection periods, payable cycles, and operational forecasts to determine whether the historical average should be adjusted.

The final working capital target is therefore not purely an accounting exercise. It is a negotiated view of what the business needs to operate normally once ownership changes.

A seller who understands this distinction enters negotiations from a far stronger position than one who treats the peg as a routine accounting schedule.

Where the Net Working Capital Peg Is Actually Negotiated

Many owners assume the negotiation ends once both sides agree on the purchase price.

In reality, some of the most meaningful negotiations begin after the letter of intent is signed. The net working capital peg often becomes one of the last major financial issues to resolve before closing because it directly determines how much operating capital the seller leaves in the business.

The discussion is rarely about the formula. Buyers and sellers usually agree on how net working capital is calculated.

The negotiation is about what represents “normal.”

That single word can move hundreds of thousands of dollars from one side of the transaction to the other.

Which Historical Period Should Be Used?

One of the first discussions is deciding how much historical data should determine the working capital peg.

A buyer may prefer the most recent twelve months because it reflects current operations.

A seller may argue that a longer period better represents the business if recent months included unusual events such as supply chain disruptions, temporary inventory shortages, or delayed customer collections.

Neither position is automatically correct.

For example:

- A mature manufacturing company with stable revenue may justify a trailing twelve-month average.

- A business with significant seasonality may require eighteen or twenty-four months to capture a complete operating cycle.

- A company that recently completed a major expansion may argue that historical averages no longer reflect its current operating needs.

The goal should not be to find the period that produces the most favorable number. The goal should be to identify the period that best reflects the capital required to operate the business under normal conditions.

Experienced deal teams spend considerable time validating this assumption because every subsequent calculation depends on it.

Growth Creates One of the Biggest Negotiation Challenges

Historical averages become less reliable when the business is growing rapidly.

Imagine revenue has increased from $10 million to $15 million during the past year.

Receivables have grown.

Inventory levels have increased.

Supplier balances have expanded.

Using an average from earlier months may understate the amount of operating capital required to support the larger business.

Buyers often argue that the net working capital target should reflect the company’s current size rather than its historical average.

Sellers typically respond that they should not be required to finance future growth for the buyer.

Both arguments have merit.

The answer usually comes from analyzing operational metrics rather than relying solely on accounting balances.

Advisors often review:

- Days Sales Outstanding (DSO)

- Inventory turnover

- Days Payable Outstanding (DPO)

- Monthly revenue growth

- Gross margin trends

- Purchasing cycles

These metrics provide context for whether the historical working capital profile still reflects how the business operates today.

Deferred Revenue Often Creates Different Expectations

Deferred revenue can become one of the more nuanced discussions, particularly for software companies, maintenance businesses, subscription services, and companies with prepaid customer contracts.

From the buyer’s perspective, deferred revenue represents future work that still needs to be performed.

From the seller’s perspective, the associated cash has already been collected.

Whether deferred revenue is included in the working capital adjustment depends largely on the purchase agreement and the economic understanding between both parties.

The important point is consistency.

If deferred revenue is included in the peg calculation, it should also be treated consistently in the closing balance sheet. Changing the treatment midway through negotiations often creates avoidable disputes during the post-closing review.

Aged Accounts Receivable Become a Credibility Test

Not every receivable deserves the same value.

A buyer reviewing the aging schedule will typically ask questions such as:

- How much is more than 90 days old?

- Which customers have disputed invoices?

- Are there balances that management does not realistically expect to collect?

If significant aged receivables remain on the balance sheet, buyers frequently argue they should not count toward normalized working capital.

Sellers sometimes respond that the receivables have historically been collectible, even if customers pay slowly.

The supporting evidence usually determines which position prevails.

Collection history, customer payment patterns, and subsequent cash receipts often carry more weight than management’s expectations alone.

Removing questionable receivables before going to market generally creates a cleaner negotiation than defending them during diligence.

Inventory Is Rarely Worth Its Book Value

Inventory discussions extend far beyond the general ledger.

Buyers want to know whether inventory is:

- Saleable

- Required for ongoing operations

- Properly valued

- Free from obsolescence

A warehouse filled with slow-moving inventory may increase reported working capital without increasing the economic value transferred to the buyer.

This is why inventory analysis often includes:

- Aging reports

- Turnover ratios

- Physical inventory observations

- Reserve calculations

- SKU-level movement analysis

Buyers frequently request additional reserves for obsolete or excess inventory.

Sellers naturally resist adjustments they believe are overly conservative.

The strongest position is usually supported by operational data rather than accounting estimates.

Accounts Payable Can Be Manipulated More Easily Than Many Sellers Realize

Accounts payable deserves just as much scrutiny as inventory.

Suppose a seller delays supplier payments during the final month before closing.

Cash increases.

Accounts payable also increases.

The business appears to have lower closing working capital, even though nothing has fundamentally changed operationally.

Buyers routinely compare payment patterns over several months to determine whether suppliers were paid consistently.

Large deviations often trigger additional questions.

If payment timing has changed simply to improve cash before closing, buyers usually adjust the calculation to reflect normal operating practices.

The same principle applies when suppliers are paid unusually early.

Accelerated payments can artificially increase the apparent working capital requirement and may also become a point of negotiation.

The Quality of Earnings Review Often Shapes the Peg

One of the biggest misconceptions is that the Quality of Earnings (QoE) review only validates EBITDA.

In practice, QoE findings frequently influence the net working capital peg as well.

During a QoE review, advisors examine whether working capital reflects recurring operating activity or temporary accounting distortions.

Common findings include:

- Revenue recognized before performance obligations are complete.

- One-time customer deposits.

- Inventory reserves that no longer reflect actual conditions.

- Accrued liabilities that should be adjusted.

- Changes in accounting policies between reporting periods.

These findings often become negotiation points when establishing the working capital target.

A buyer who identifies weak reserves or inconsistent accounting policies may argue for a higher peg or additional adjustments.

A seller who has already identified and addressed these issues before entering the market generally negotiates from a stronger position because fewer surprises emerge during diligence.

This is one reason a thorough working capital due diligence process is valuable before signing the purchase agreement.

Who Usually Wins These Negotiations?

Neither side wins every issue.

Well-managed businesses with consistent financial reporting, disciplined inventory controls, and predictable collection practices typically give sellers greater leverage because the historical numbers are easier to defend.

Businesses with inconsistent accounting, aging receivables, excess inventory, or significant month-end adjustments often leave buyers with more room to argue for changes.

The important lesson is that the net working capital peg is not determined by a spreadsheet alone.

It is negotiated through evidence.

The side that can best demonstrate what “normal” operations look like usually has the stronger position when the purchase agreement is finalized.

The Closing True-Up: Where the Purchase Price Actually Changes

Many sellers believe the purchase price becomes final once the purchase agreement is signed.

In most lower middle market transactions, that is not the case.

The enterprise value may be fixed, but the amount the seller ultimately receives often depends on the closing working capital calculation. This process is commonly known as the working capital true-up.

The purpose is simple. The buyer wants to receive the business with the agreed level of operating working capital. If the business is delivered with less than the agreed net working capital peg, the buyer receives compensation through a purchase price adjustment. If the business is delivered with more than the agreed target, the seller is typically entitled to additional proceeds.

The adjustment is designed to ensure that neither party benefits unfairly from changes in operating working capital immediately before closing.

How the True-Up Process Usually Works

Although every purchase agreement is different, the process generally follows the same sequence.

- The buyer and seller agree on a net working capital peg during negotiations.

- The transaction closes based on an estimated closing balance sheet.

- After closing, the buyer prepares the final closing balance sheet as required under the purchase agreement.

- Both parties compare the actual closing working capital against the agreed target.

- Any difference results in a post-closing adjustment to the purchase price.

The adjustment is typically dollar for dollar.

If the agreed peg is $2.4 million and the final closing working capital is $2.1 million, the seller generally owes the buyer $300,000 through the true-up process.

Likewise, if the closing working capital exceeds the target by $300,000, the seller would generally receive an additional $300,000.

The mechanics are straightforward.

The disagreements usually arise over how the closing balance sheet was prepared and whether the accounting follows the principles established in the purchase agreement.

A Practical Example of a Net Working Capital True-UpThe following example is for illustration only.

A manufacturing company agrees to sell for an enterprise value of $15,000,000.

After reviewing twenty-four months of historical financial statements, both parties agree on a net working capital peg of $2,750,000.

The purchase agreement states that the final purchase price will be adjusted based on the actual closing working capital.

On the closing date, the estimated balance sheet shows:

| Item | Amount |

| Accounts Receivable | $2,950,000 |

| Inventory | $1,650,000 |

| Other Operating Current Assets | $250,000 |

| Accounts Payable | ($1,650,000) |

| Accrued Operating Liabilities | ($850,000) |

| Closing Net Working Capital | $2,350,000 |

The agreed working capital target was $2,750,000.

Actual closing working capital is $400,000 below the agreed peg.

The result is:

Purchase Price Adjustment = -$400,000

Instead of receiving proceeds based on the original transaction value, the seller’s final proceeds are reduced by $400,000.

Nothing changed about the company’s valuation.

Nothing changed about the negotiated EBITDA multiple.

The reduction occurred solely because the business was delivered with less operating working capital than both parties agreed.

Where Sellers Commonly Lose Money During the True-Up

Most purchase price adjustments are not caused by arithmetic mistakes.

They occur because the parties disagree about what belongs in the closing balance sheet.

Some of the most common issues include:

Inventory Reserves

The buyer concludes that certain inventory items are obsolete or slow moving and increases the reserve.

That reduces inventory.

Lower inventory reduces closing working capital.

The seller’s proceeds decline.

Uncollectible Accounts Receivable

Receivables that appeared collectible during negotiations may no longer satisfy the buyer’s collection assumptions after closing.

If additional bad debt reserves are recorded, working capital falls.

Accrued Expenses

Bonuses, warranty obligations, payroll accruals, vacation liabilities, or customer rebates may not have been fully reflected before closing.

Higher accrued liabilities reduce working capital.

Changes in Accounting Policies

The purchase agreement often requires the closing balance sheet to follow the company’s historical accounting policies.

Disagreements arise when buyers introduce more conservative reserve methodologies or apply accounting treatments that differ from historical practice.

Well-drafted purchase agreements specify the accounting principles to avoid these disputes.

Timing Differences

A large customer payment received one day earlier or one day later can materially change accounts receivable.

Likewise, paying suppliers immediately before closing changes accounts payable.

Although these timing differences appear small individually, together they can materially affect the working capital adjustment.

The Purchase Agreement Matters as Much as the Calculation

Many owners assume the financial analysis determines the outcome.

In practice, the purchase agreement often has the final word.

A carefully drafted agreement should clearly define:

- The methodology used to calculate net working capital.

- Which accounts are included or excluded.

- The accounting policies that govern the closing balance sheet.

- How disputed items will be resolved.

- The timeline for preparing the final true-up.

- The dispute resolution process if both parties cannot agree.

The clearer these provisions are before closing, the less likely the transaction will end in a lengthy post-closing dispute.

Advisor’s Take

Business owners often ask when they should begin thinking about the net working capital peg.

Many assume it becomes important after they receive a Letter of Intent.

That is usually too late.

By the time a buyer begins financial diligence, the historical balance sheet already tells a story.

If inventory has been poorly managed for years, receivables contain long-outstanding balances, or liabilities fluctuate significantly from month to month, those patterns will almost certainly become negotiation points.

The strongest sellers prepare well before going to market.

They review working capital trends over at least the previous twelve months.

They identify unusual balances that require explanation.

They write off inventory that is no longer saleable.

They clean up aging receivables that are unlikely to be collected.

They ensure accruals are complete and consistent.

Preparing the balance sheet early gives sellers time to improve operations rather than defend avoidable issues during diligence.

Businesses that proactively address these areas through proper preparation before going to market generally enter negotiations with stronger evidence and fewer surprises.

At the same time, sellers should avoid becoming obsessed with negotiating the lowest possible peg.

That is often the wrong objective.

Sophisticated buyers rarely object to a reasonable peg supported by historical performance.

They do object to calculations that appear engineered to maximize proceeds.

The better strategy is to establish a peg that accurately reflects normal operating requirements and is supported by consistent financial reporting.

A defensible peg creates credibility.

Credibility often leads to faster negotiations, fewer disputes during the working capital true-up, and greater confidence that the purchase price agreed today will remain substantially intact when the transaction finally closes.

Frequently Asked Questions

How Is a Net Working Capital Peg Determined?

A net working capital peg is typically determined by analyzing the company’s historical operating working capital over the previous twelve months. For businesses with significant seasonality or rapid growth, buyers and sellers may review eighteen or twenty-four months of financial data instead. The historical balances are then normalized by removing one-time or non-operating items to establish the amount of working capital the business normally requires to operate. The agreed figure becomes the working capital target against which the closing balance sheet is measured.

What Is a Working Capital True-Up?

A working capital true-up is the post-closing process used to compare the actual closing working capital delivered by the seller against the agreed net working capital peg. If the business is transferred with less working capital than the agreed target, the purchase price is typically reduced on a dollar-for-dollar basis. If the business delivers more than the target, the seller may receive additional proceeds. The true-up ensures that neither party gains an unintended financial advantage from changes in operating working capital immediately before closing.

Why Can a Net Working Capital Peg Reduce My Sale Price?

The net working capital peg does not change the agreed enterprise value of the business. Instead, it determines whether the seller has transferred the expected level of operating working capital at closing. If actual working capital falls below the agreed target because of lower inventory, slower customer collections, higher accrued liabilities, or other balance sheet changes, the buyer is effectively required to contribute additional operating capital after the acquisition. Most purchase agreements compensate the buyer through a corresponding purchase price adjustment, reducing the seller’s final proceeds.

Final Thoughts

For many business owners, the net working capital peg receives far less attention than valuation or EBITDA multiples. That is often a costly mistake.

A well-negotiated purchase price can still be reduced if the working capital target is poorly defined or if the closing balance sheet does not reflect the level of operating capital promised in the purchase agreement. In lower middle market transactions, disputes over inventory, accounts receivable, accrued liabilities, and accounting policies routinely influence the final amount a seller receives.

The strongest sellers begin preparing long before the business goes to market. They understand their working capital trends, normalize unusual balance sheet items, and support every assumption with reliable financial data. That preparation not only strengthens negotiations but also reduces the likelihood of a difficult post-closing true-up.

If you are preparing to sell your business or reviewing a Letter of Intent, understanding how the net working capital peg is established can help protect your proceeds and avoid costly surprises at closing.

If you would like an experienced M&A team to review your transaction, assess your working capital position, or identify potential purchase price risks before negotiations begin.

Schedule a confidential consultation with Horizon M&A Advisors