Sellers Think These EBITDA Adjustments Are Safe. Buyers Often Don’t.

A single EBITDA adjustment can look harmless until an independent Quality of Earnings review challenges it.

What surprises many business owners is that buyers rarely remove the aggressive adjustments first. They remove the ones sellers believed were already settled.

Owner compensation, recurring expenses labeled as one-time, personal expenses without sufficient documentation, related-party rent, discretionary spending, and unsupported run-rate projections are among the EBITDA adjustments most commonly rejected. When those adjustments disappear, Normalized EBITDA falls, and the purchase price often falls with it.

Key Takeaways

If you only remember four things from this article, remember these:

- Most valuation reductions happen because buyers challenge EBITDA adjustments, not because they lower the valuation multiple.

- Buyers care less about your explanation and more about whether an independent accountant can verify the adjustment.

- Every dollar removed from Normalized EBITDA can reduce enterprise value by five to eight dollars in a typical lower middle market transaction.

- The strongest EBITDA adjustments are supported by documentation, historical consistency, and market evidence.

Why This Matters More Than Most Sellers Realize

Many business owners believe the negotiation ends once the Letter of Intent is signed.

In reality, that is when buyers begin testing the financial story behind the numbers.

One of the first questions a Quality of Earnings provider asks is simple:

“Can every EBITDA adjustment be independently verified?”

If the answer is no, the discussion quickly shifts from valuation to credibility.

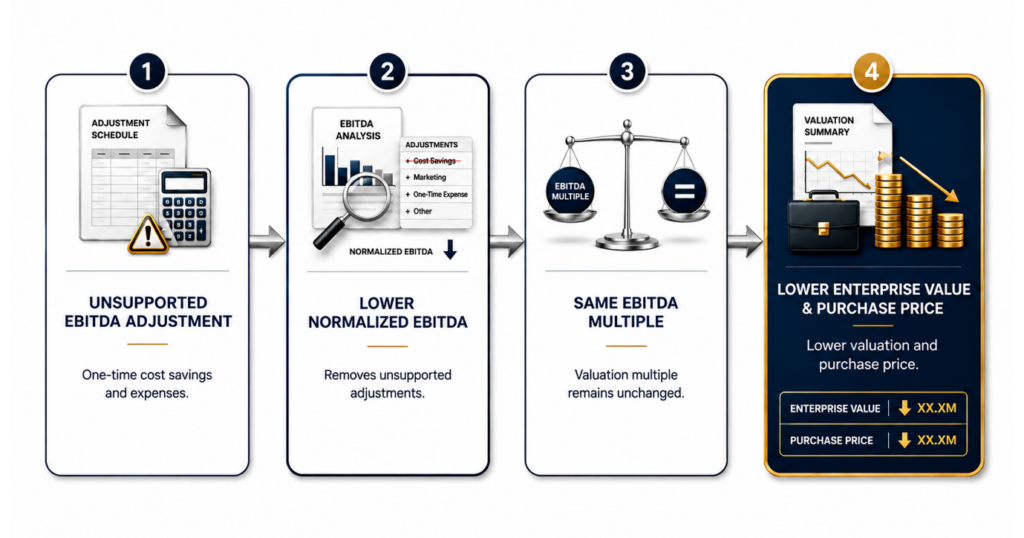

Consider a business with $3.5 million of Adjusted EBITDA that receives an offer at a 6.5x multiple.

During the Quality of Earnings review, the buyer removes $200,000 of unsupported EBITDA adjustments.

The buyer never changes the multiple.

Instead, they apply the same 6.5x multiple to a lower EBITDA figure.

That single adjustment reduces the purchase price by approximately:

$200,000 × 6.5 = $1.3 million

That is why experienced buyers spend weeks reviewing adjustments that sellers often expect to pass without debate.

When financial assumptions cannot survive a thorough Quality of Earnings review, sellers often face one of three outcomes:

- The buyer asks for a purchase price reduction.

- The parties enter difficult renegotiations that delay closing.

- Confidence in the deal weakens enough that the transaction never reaches the finish line.

This is also why a professional business valuation should never rely solely on management-adjusted numbers. Buyers ultimately pay for sustainable earnings, not optimistic assumptions.

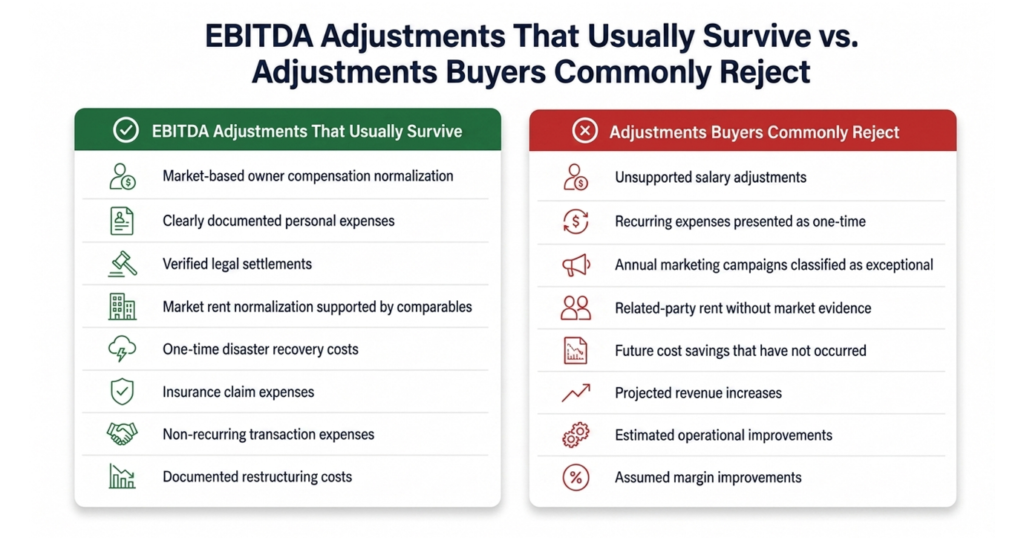

Which EBITDA Adjustments Usually Survive a Quality of Earnings Review?

After sitting through enough sell-side transactions, one pattern becomes obvious.

Buyers are not looking for reasons to reject every adjustment.

They are looking for adjustments that cannot survive independent verification.

The strongest EBITDA adjustments usually share three characteristics:

- They are clearly non-recurring.

- They are fully documented.

- They have little room for interpretation.

The weakest adjustments rely on management’s expectations rather than historical evidence.

The table below reflects the kinds of adjustments that consistently survive Quality of Earnings reviews and the ones that frequently become negotiation points.

The difference between these two columns is rarely accounting knowledge.

It is evidence.

The EBITDA Adjustments Buyers Challenge Most Often

The biggest misconception sellers have is that buyers are looking for aggressive add-backs.

In my experience, that is rarely true.

Most buyers expect some level of EBITDA normalization. What they question is whether each adjustment represents a genuine, sustainable increase in earnings or simply a more favourable way of presenting historical results.

The difference usually comes down to evidence.

1. Owner Compensation Normalization

This is one of the most common EBITDA adjustments and one of the easiest to justify when handled correctly.

Many privately held businesses pay owners significantly more or less than a market-rate executive.

Suppose the owner earns $450,000 annually, but an independent CEO performing the same role would likely earn $220,000.

A buyer will often accept a $230,000 EBITDA adjustment because the excess compensation would not continue after the acquisition.

Where sellers lose credibility is when they assume every dollar above their preferred salary automatically becomes an add-back.

Buyers typically ask questions such as:

- What would it cost to replace the owner’s responsibilities?

- Does the business require multiple executives instead of one?

- Are family members performing legitimate operational roles?

- Is there third-party compensation data supporting the adjustment?

The strongest owner compensation adjustments are supported by salary surveys, industry benchmarks, payroll records, and clearly defined management responsibilities.

The weakest rely solely on management’s opinion.

2. Personal Expenses Run Through the Business

Nearly every privately owned company has some level of discretionary personal spending.

That alone does not concern buyers.

Poor documentation does.

Examples commonly reviewed during a Quality of Earnings Analysis include:

- Personal vehicle leases

- Family vacations

- Home internet and utilities

- Club memberships

- Private school tuition

- Personal insurance

- Non-business meals

- Luxury travel

Many of these expenses can qualify as legitimate EBITDA Add Backs.

However, buyers increasingly request supporting invoices, credit card statements, and general ledger details.

If an expense cannot be clearly separated from legitimate business activity, buyers often remove all or part of the adjustment.

One unsupported expense may not materially affect valuation.

Several unsupported adjustments can reduce confidence in the entire financial package.

3. “One-Time” Expenses That Keep Happening

This is where many sellers unintentionally overstate Adjusted EBITDA.

The phrase “one-time expense” sounds straightforward.

In practice, buyers evaluate patterns rather than labels.

Suppose a business reports:

- Recruiting costs in 2023

- Recruiting costs again in 2025

- Executive search fees expected next year

Those expenses are no longer truly one-time.

The same applies to:

- Annual litigation

- Marketing campaigns

- ERP implementation projects

- Equipment repairs

- Consulting engagements

- Cybersecurity upgrades

A useful rule during Quality of Earnings Reviews is simple:

If something happens regularly, buyers usually treat it as part of normal operations.

The adjustment disappears.

4. Related-Party Rent

Real estate often creates one of the largest valuation debates in privately held companies.

Many owners operate from property owned through a separate LLC.

Sometimes the business pays below-market rent.

Sometimes it pays above-market rent.

Neither figure matters very much.

Buyers care about market rent because that reflects the operating economics of the business after closing.

For example:

Current rent paid:

$90,000 per year

Independent market analysis:

$180,000 per year

Even though the seller historically benefited from below-market rent, the buyer will typically normalize occupancy costs to current market rates.

The result may actually reduce EBITDA.

This surprises many sellers because they assumed the existing lease protected the adjustment.

It does not.

5. Discretionary Spending

Discretionary spending occupies a gray area between legitimate business expense and owner lifestyle.

Examples include:

- Country club memberships

- Executive entertainment

- Sponsorships with little commercial value

- Luxury vehicles

- Personal charitable donations

- Family payroll

- High-end travel

Some of these expenses qualify as valid EBITDA Adjustments.

Others do not.

The deciding question is rarely:

“Would the new owner spend this money?”

Instead, buyers ask:

“Would a reasonable operator need this expense to generate the company’s current earnings?”

That distinction changes many Quality of Earnings Reports.

6. Pro Forma and Run-Rate Adjustments

If there is one category that consistently creates difficult conversations, it is projected future performance.

Examples include:

- “The new production line will improve margins.”

- “We’ve already hired another salesperson.”

- “The new customer contract begins next quarter.”

- “Material costs should fall next year.”

From a seller’s perspective, these assumptions may feel inevitable.

From a buyer’s perspective, they remain forecasts.

Most Quality of Earnings providers require historical evidence before recognizing these improvements.

Unless the increased earnings have already appeared in the financial statements or are contractually guaranteed, buyers usually reject the adjustment.

One experienced buyer summarized it this way during a transaction:

“Hope is not an EBITDA adjustment.”

That sentence has stayed with me because it captures how disciplined buyers think.

Common Documentation That Strengthens EBITDA Adjustments

Well-supported adjustments survive scrutiny far more often than poorly documented ones.

Before going to market, sellers should expect buyers to request evidence such as:

| EBITDA Adjustment | Documentation Buyers Want to See |

| Owner compensation | Payroll records, salary benchmarks, job descriptions |

| Personal expenses | Invoices, receipts, general ledger entries |

| Related-party rent | Independent market lease comparisons |

| One-time legal expenses | Settlement agreements and invoices |

| Insurance claims | Claim documentation and reimbursement records |

| Restructuring costs | Board approvals, contracts, payment records |

The businesses that experience the smoothest diligence process are rarely those with the highest EBITDA.

They are the ones with the strongest documentation.

A Deal Breakdown: How a Quality of Earnings Review Changed the ValuationA manufacturing business entered buyer exclusivity with Adjusted EBITDA of $2.80 million.

Management included several EBITDA adjustments that had been accepted internally for years.

The buyer’s accounting firm completed its Quality of Earnings Review and challenged two adjustments.

Adjustment One

Management added back $250,000 of projected labor savings from consolidating two production facilities.

The consolidation plan was approved but had not yet been implemented.

The buyer rejected the adjustment because no historical financial results demonstrated the savings.

Adjustment Two

Management also classified $100,000 of consulting expenses as one-time.

During diligence, invoices showed nearly identical consulting engagements had occurred in three of the previous five years.

The buyer determined those costs were recurring operating expenses.

The final calculation looked like this:

| Item | EBITDA |

| Seller’s Adjusted EBITDA | $2,800,000 |

| Remove projected labor savings | -$250,000 |

| Remove recurring consulting expenses | -$100,000 |

| Buyer’s Normalized EBITDA | $2,450,000 |

The agreed purchase multiple remained 6.5x.

Nothing changed except EBITDA.

The impact on enterprise value was immediate.

| Calculation | Value |

| Seller valuation | $18.20 million |

| Buyer valuation | $15.93 million |

| Reduction in purchase price | $2.27 million |

The negotiation that followed was not about accounting.

It was about evidence.

By the end of diligence, both parties agreed on the valuation multiple.

The only disagreement was what the business actually earned.

That is why the quality of your EBITDA adjustments matters just as much as the quality of your business.

Advisor’s Take: Don’t Build Your Valuation Around EBITDA Adjustments You Can’t Defend

After advising business owners through lower middle market transactions, I’ve noticed a pattern.

The deals that close with the fewest surprises are rarely the ones with the highest Adjusted EBITDA.

They’re the ones where every EBITDA adjustment can withstand independent scrutiny.

Too many sellers spend months trying to maximize EBITDA before going to market. They search for every possible add-back, hoping to present the strongest financial picture.

That approach often backfires.

Once a buyer’s accounting firm begins its Quality of Earnings Analysis, unsupported adjustments become more than accounting issues. They become credibility issues.

When buyers discover one questionable adjustment, they naturally begin asking whether the rest of the financial story is equally optimistic.

I’ve seen transactions where a single weak adjustment led buyers to request additional diligence, expand document requests, or challenge adjustments that would otherwise have been accepted.

The discussion shifts from numbers to trust.

Trust is difficult to rebuild once it’s lost.

Focus on Defensible EBITDA Adjustments, Not Every Possible Adjustment

Before taking your business to market, review every adjustment as if you were the buyer’s accounting firm.

Ask yourself:

- Can I produce documentation supporting this adjustment within five minutes?

- Would an independent CPA reach the same conclusion?

- Has this expense truly disappeared from the business?

- Would this adjustment still make sense if I removed my personal knowledge of the company?

If any answer is “no,” assume the buyer will question it.

That doesn’t necessarily mean the adjustment is invalid.

It means you need stronger evidence before relying on it during negotiations.

The businesses that experience the smoothest transactions usually begin preparing their business for sale months before approaching buyers. They organize financial records, clean up discretionary spending, normalize owner compensation, and document unusual expenses before Quality of Earnings begins.

The objective is not simply to increase EBITDA.

It is to make every adjustment believable.

What Is Usually Worth the Effort?

In my experience, sellers receive the greatest return from preparing adjustments that buyers already expect to see.

These typically include:

- Owner compensation supported by market salary data

- Clearly documented personal expenses

- Verifiable one-time legal settlements

- Insurance claims

- Market-rate rent supported by comparable leases

- Transaction-related professional fees

These adjustments are generally straightforward because independent evidence exists.

What Usually Isn’t Worth Fighting Over?

Some adjustments create far more debate than value.

Examples include:

- Future cost savings that haven’t occurred

- Expected revenue from new customers

- Projected margin improvements

- Estimated operational efficiencies

- Expenses labeled as “one-time” despite occurring regularly

- Aggressive management assumptions

These adjustments often consume significant time during diligence and rarely change the buyer’s position.

If an adjustment depends on explaining why it should happen rather than proving it did happen, it is probably too aggressive.

The Question Every Seller Should Ask Before Going to Market

Before your financial statements ever reach a buyer, ask yourself one simple question:

“If an independent Quality of Earnings firm reviewed every EBITDA adjustment tomorrow, which ones would survive without me being in the room to explain them?”

That answer usually tells you more about your valuation than any spreadsheet.

The strongest negotiations begin long before the Letter of Intent is signed.

They begin with financial statements that can withstand scrutiny.

If you’re still preparing for an eventual sale, thoughtful exit planning gives you time to identify weak adjustments, improve documentation, and present a more credible financial picture before buyers begin diligence.

Common Mistakes Sellers Make With EBITDA Adjustments

The following mistakes appear in transactions far more often than most business owners realize.

Mistake 1: Treating Every Owner Expense as an Add Back

Not every expense the owner personally benefits from qualifies as an EBITDA adjustment.

Buyers expect documentation and a clear business rationale.

Mistake 2: Calling Recurring Costs “One-Time”

If similar expenses appear every year or every few years, buyers usually classify them as normal operating expenses.

Changing the label doesn’t change the history.

Mistake 3: Including Future Savings That Haven’t Happened

Projected efficiencies may improve the business later.

They rarely improve today’s valuation.

Buyers pay for demonstrated earnings, not expected earnings.

Mistake 4: Waiting Until Due Diligence to Explain Adjustments

By the time Quality of Earnings begins, buyers expect answers, not discoveries.

Supporting documentation should already exist before the business goes to market.

Seller Preparation Checklist Before a Quality of Earnings Review

Use this checklist before sharing financial information with prospective buyers.

- Document every EBITDA adjustment with supporting evidence.

- Benchmark owner compensation against comparable market salaries.

- Separate personal expenses from legitimate business expenses.

- Review recurring expenses that may have been classified as one-time.

- Obtain market support for related-party rent adjustments.

- Remove speculative run-rate assumptions that cannot be verified.

- Prepare explanations that are supported by documents rather than memory.

- Review your financial statements from the perspective of an independent accounting firm.

Completing this work before buyers begin diligence often leads to smoother negotiations, fewer retrades, and greater confidence throughout the transaction.

Frequently Asked Questions

What are EBITDA adjustments?

EBITDA adjustments are changes made to reported EBITDA to reflect the company’s sustainable earning power. Common adjustments include owner compensation normalization, non-recurring legal expenses, personal expenses run through the business, and other items that are unlikely to continue after a sale.

Why do buyers reject EBITDA adjustments during a Quality of Earnings review?

Buyers reject EBITDA adjustments when they cannot verify them with documentation or believe the expense is recurring rather than one-time. A Quality of Earnings review focuses on sustainable profitability, not management assumptions.

What is the difference between EBITDA and Adjusted EBITDA?

EBITDA measures earnings before interest, taxes, depreciation, and amortization. Adjusted EBITDA starts with EBITDA and then adds back certain non-recurring or discretionary expenses to estimate the company’s normalized operating earnings. Buyers carefully evaluate whether those adjustments are justified before accepting them.

Do all personal expenses qualify as EBITDA add backs?

No. Personal expenses can qualify only when they are clearly unrelated to business operations and supported by documentation such as invoices, payroll records, or accounting entries. Unsupported or mixed-use expenses are frequently challenged during Quality of Earnings reviews.

What documentation supports EBITDA adjustments?

The strongest support includes payroll records, general ledger reports, invoices, lease agreements, insurance claims, legal settlement documents, salary benchmarking studies, and third-party market data. Buyers are far more likely to accept adjustments backed by objective evidence than management explanations.

Can rejected EBITDA adjustments reduce the purchase price even if the valuation multiple stays the same?

Yes. This is one of the most common outcomes during sell-side transactions. If buyers remove unsupported EBITDA adjustments, Normalized EBITDA decreases. Applying the same valuation multiple to a lower EBITDA results in a lower enterprise value and, ultimately, a lower purchase price.

Final Thoughts

Quality of Earnings is rarely about finding accounting mistakes.

It’s about determining whether the earnings a buyer is paying for will still exist after closing.

The sellers who achieve the strongest outcomes aren’t necessarily the ones with the highest Adjusted EBITDA.

They’re the ones whose EBITDA adjustments are transparent, well-documented, and supported by evidence that stands on its own.

When your financial story can withstand independent scrutiny, negotiations become simpler, buyer confidence increases, and your valuation is far more likely to hold from the Letter of Intent to closing.

Not Sure Whether Your EBITDA Adjustments Will Survive Buyer Scrutiny?

If you’re preparing to sell your business, it’s worth identifying potential issues before a buyer’s accounting team does.

Our advisors work with business owners to review EBITDA adjustments, identify areas buyers are likely to challenge, and help prepare financial information that stands up during a Quality of Earnings review.

Schedule a confidential consultation to discuss your business and understand how your financials may be viewed by prospective buyers.