Selling a business isn’t just about finding a buyer-it’s about convincing them your company is worth paying a premium for. While many owners focus on growing revenue, experienced buyers look much deeper. Their attention quickly turns to one financial metric: EBITDA.

EBITDA helps buyers evaluate how much profit a business generates from its core operations before financing decisions, taxes, and certain accounting expenses come into play. More importantly, buyers rarely rely on the EBITDA reported in your financial statements. Instead, they adjust and normalize it to determine the company’s true earning power.

Understanding how this process works can make a significant difference in your business valuation. In this guide, you’ll learn what EBITDA is, how buyers calculate it, why normalized EBITDA matters, and what you can do before going to market to maximize your company’s value.

What Is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is one of the most widely used financial metrics in mergers and acquisitions because it focuses on a company’s operating performance rather than accounting or financing decisions.

In simple terms, EBITDA measures how much profit a business generates from its day-to-day operations before considering:

- Interest on loans

- Income taxes

- Depreciation of physical assets

- Amortization of intangible assets

These expenses can vary significantly from one company to another, making direct comparisons difficult. By excluding them, buyers can compare businesses on a more consistent basis.

For example, two manufacturing companies may generate identical operating profits, but one may report lower net income simply because it has more debt or recently invested in expensive equipment. EBITDA removes those differences, allowing buyers to evaluate the underlying strength of each business.

This is why EBITDA has become the foundation for many business valuation methods, particularly in the lower middle market. Buyers, investors, private equity firms, and lenders often begin their financial analysis with EBITDA before applying valuation multiples or conducting deeper due diligence.

How Is EBITDA Calculated?

The most common EBITDA formula starts with Net Income and adds back expenses that do not directly reflect a company’s operating performance.

EBITDA Formula

EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization

Let’s break each component down:

| Component | What It Represents |

| Net Income | Profit after all expenses |

| Interest | Cost of business debt |

| Taxes | Income tax expense |

| Depreciation | Non-cash expense for tangible assets |

| Amortization | Non-cash expense for intangible assets |

EBITDA Calculation Example

Imagine a business reports the following annual financial results:

| Item | Amount |

| Net Income | $900,000 |

| Interest Expense | $120,000 |

| Taxes | $180,000 |

| Depreciation | $150,000 |

| Amortization | $50,000 |

EBITDA = $1,400,000

This figure gives buyers a clearer view of the company’s operating profitability before financing structure and accounting treatments influence the results.

Why the Formula Matters

Many business owners assume that higher revenue automatically translates into a higher valuation. In reality, buyers are far more interested in how efficiently your business converts revenue into sustainable earnings.

A company generating $15 million in annual revenue with weak EBITDA may be worth less than a business producing $8 million in revenue but consistently delivering strong operating profits. That’s why EBITDA often carries more weight than top-line sales during acquisition discussions.

Why Buyers Use EBITDA Instead of Net Profit

One of the biggest surprises for business owners is that buyers rarely value a company based on net profit. Instead, EBITDA serves as the primary benchmark because it provides a clearer picture of a business’s operating performance and future earning potential.

While net profit is an important accounting metric, it can be heavily influenced by financing decisions, tax strategies, and non-cash expenses that don’t necessarily reflect how well the business is performing.

For example, imagine two distribution companies generate the same annual revenue and have similar operating costs. One company financed new equipment with debt, resulting in high interest expenses, while the other purchased equipment outright. Their net profits may look very different, even though their core operations are equally profitable.

EBITDA removes these variables, allowing buyers to compare businesses on a more consistent basis.

Why EBITDA Matters to Buyers

During an acquisition, buyers ask one fundamental question:

“How much sustainable operating profit will this business generate after I take ownership?”

EBITDA helps answer that question by focusing on earnings from normal business operations rather than owner-specific financial decisions.

Buyers rely on EBITDA because it helps them:

- Compare companies with different capital structures.

- Evaluate operational performance across competitors.

- Remove the impact of financing and tax strategies.

- Estimate future cash-generating ability.

- Apply valuation multiples consistently.

- Assess whether the acquisition can support future debt or investment.

Ultimately, buyers are investing in future earnings, not historical accounting profits.

Buyer Perspective

Think like an acquirer.

Buyers aren’t purchasing your past-they’re purchasing your company’s ability to generate reliable earnings in the future. That’s why they spend significant time validating the quality and sustainability of EBITDA before discussing valuation.

EBITDA vs. Net Profit

| EBITDA | Net Profit |

| Measures operating performance | Measures final accounting profit |

| Excludes interest, taxes, depreciation, and amortization | Includes all expenses |

| Commonly used in M&A valuations | Used primarily for financial reporting |

| Easier to compare across businesses | Influenced by financing and tax decisions |

| Focuses on earning potential | Reflects historical accounting results |

EBITDA Isn’t the Whole Story

Although EBITDA is one of the most important valuation metrics, buyers don’t stop there.

Before determining a purchase price, they also evaluate:

- Customer concentration

- Revenue quality

- Gross margins

- Recurring revenue

- Industry outlook

- Management team strength

- Working capital requirements

- Capital expenditure needs

- Growth opportunities

- Operational risks

A business with strong EBITDA but significant customer concentration or inconsistent financial reporting may still receive a lower valuation than expected.

Adjusted EBITDA vs. Normalized EBITDA

One of the most misunderstood aspects of business valuation is the difference between Adjusted EBITDA and Normalized EBITDA.

Many business owners use these terms interchangeably. While they are closely related, buyers and professional M&A advisors make an important distinction between the two.

Understanding this difference can significantly impact your company’s valuation.

What Is Adjusted EBITDA?

Adjusted EBITDA starts with reported EBITDA and adds back expenses or income that are considered unusual, discretionary, or non-operating.

These adjustments aim to present a clearer picture of operating performance by removing items that are unlikely to continue after the sale.

Common seller add-backs include:

- Owner compensation above market rates

- Personal vehicle expenses

- Personal travel charged to the business

- Family members on payroll without active roles

- One-time legal settlements

- Business relocation costs

- Major one-time repairs

- Pandemic-related expenses

- Non-operating investment income

These adjustments can increase EBITDA-but only if they are well documented and justifiable.

What Is Normalized EBITDA?

Normalized EBITDA goes one step further.

Rather than simply adding back certain expenses, it estimates the company’s true, sustainable earning power under normal operating conditions.

In other words, it answers the question:

“What level of EBITDA can a new owner reasonably expect after acquiring this business?”

Professional buyers, lenders, and Quality of Earnings (QoE) providers focus on normalized EBITDA because it reflects recurring profitability rather than temporary accounting adjustments.

Adjusted EBITDA vs. Normalized EBITDA

| Adjusted EBITDA | Normalized EBITDA |

| Removes unusual or discretionary expenses | Reflects sustainable future earnings |

| Prepared by the seller or advisor | Independently validated during due diligence |

| May include optimistic assumptions | Based on evidence and recurring operations |

| Used during initial marketing | Used by buyers to determine valuation |

Before-and-After EBITDA Example

Suppose a business reports:

Reported EBITDA:$1,800,000

During the sale process, the advisor identifies several legitimate adjustments.

| Adjustment | Amount |

| Excess Owner Salary | +$250,000 |

| Personal Vehicle & Travel Expenses | +$90,000 |

| One-Time Legal Fees | +$60,000 |

Normalized EBITDA = $2,200,000

If buyers agree these adjustments are appropriate and apply a 6× EBITDA multiple, the impact is substantial.

| Scenario | Enterprise Value |

| Reported EBITDA ($1.8M × 6) | $10.8 Million |

| Normalized EBITDA ($2.2M × 6) | $13.2 Million |

Difference in Valuation: $2.4 Million

This example demonstrates why preparing accurate EBITDA adjustments before going to market can have a meaningful impact on business value.

Which Add-Backs Do Buyers Accept?

Not every adjustment is automatically accepted.

Sophisticated buyers-and especially Quality of Earnings reviewers-scrutinize every add-back to determine whether it truly reflects a one-time or owner-specific expense.

Commonly Accepted Add-Backs

- Excess owner compensation

- Personal expenses paid by the business

- Non-recurring legal costs

- One-time consulting fees

- Business relocation expenses

- Unusual repairs caused by isolated events

- Asset impairment charges

- One-time restructuring costs

Frequently Challenged Add-Backs

- Regular maintenance expenses

- Ongoing marketing costs

- Normal employee payroll

- Routine software subscriptions

- Estimated future cost savings

- Unsupported management adjustments

- Recurring operating expenses disguised as one-time items

The more evidence you can provide for each adjustment, the more confidence buyers will have in your financial statements.

Expert Tip: Prepare supporting documentation for every proposed add-back before entering the market. Clear documentation reduces buyer skepticism, minimizes due diligence questions, and helps preserve valuation during negotiations.

How EBITDA Affects Business Valuation

Once buyers establish a credible Normalized EBITDA, the next step is determining what the business is worth.

This is where EBITDA multiples come into play.

Rather than valuing a company based solely on its assets or annual revenue, buyers often calculate its Enterprise Value (EV) using a multiple of EBITDA.

Enterprise Value Formula

Enterprise Value = Normalized EBITDA × EBITDA Multiple

The EBITDA multiple represents how much buyers are willing to pay for each dollar of sustainable operating earnings.

For example, if a company generates $3 million in Normalized EBITDA and comparable businesses in the industry trade at a 6× EBITDA multiple, the estimated Enterprise Value would be:

$3,000,000 × 6 = $18,000,000

However, the multiple isn’t fixed. It varies depending on several factors that influence risk, growth potential, and future profitability.

What Influences an EBITDA Multiple?

Buyers evaluate much more than financial performance. Factors that can increase-or decrease-the multiple include:

| Higher Multiples | Lower Multiples |

| Recurring revenue | Heavy reliance on one-time sales |

| Diversified customer base | High customer concentration |

| Strong management team | Owner-dependent operations |

| Consistent revenue growth | Declining or volatile sales |

| Healthy EBITDA margins | Thin or inconsistent margins |

| Modern systems and processes | Outdated technology or inefficient operations |

| Strong market position | Highly competitive or shrinking markets |

Even a company with strong EBITDA may receive a lower multiple if buyers perceive significant operational or market risks.

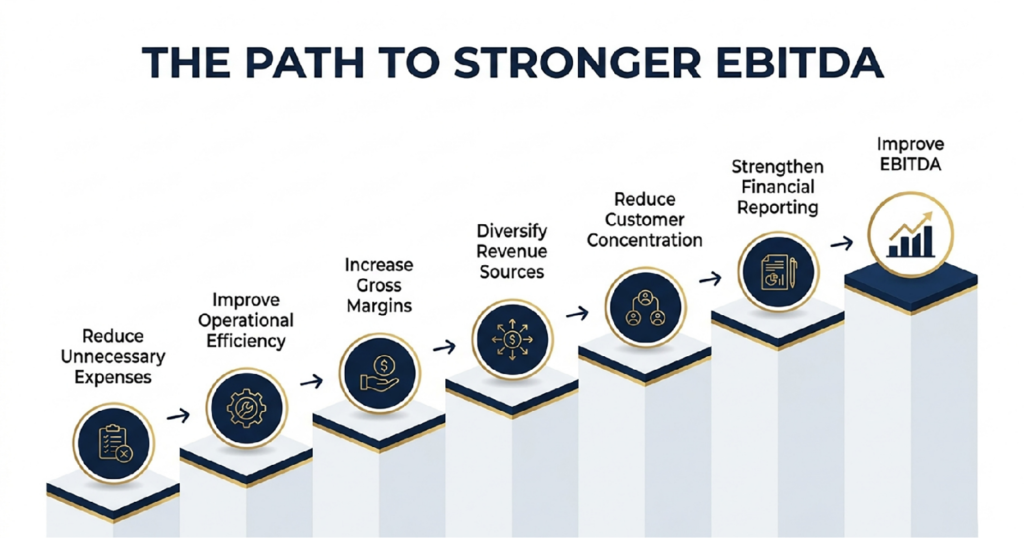

7 Ways to Improve EBITDA Before Selling Your Business

Maximizing your company’s value begins well before you decide to sell. Buyers reward businesses with sustainable earnings, efficient operations, and reliable financial reporting.

Here are seven practical ways to strengthen EBITDA before going to market.

1. Eliminate Unnecessary Expenses

Review your financial statements for discretionary spending that doesn’t contribute to business operations.

Examples include:

- Personal expenses

- Excess travel

- Duplicate software subscriptions

- Non-essential memberships

- Underutilized assets

Reducing unnecessary costs can improve operating profitability while simplifying future EBITDA adjustments.

2. Improve Operational Efficiency

Operational improvements often have a lasting impact on EBITDA.

Consider:

- Automating repetitive processes

- Improving inventory management

- Reducing production waste

- Streamlining workflows

- Renegotiating supplier agreements

Small efficiency gains can compound into meaningful profitability improvements over time.

3. Increase Gross Margins

Higher revenue doesn’t always translate into higher earnings.

Instead, focus on improving profitability by:

- Adjusting pricing strategies

- Reducing direct costs

- Selling higher-margin products or services

- Eliminating low-margin offerings

Even modest margin improvements can significantly increase EBITDA.

4. Diversify Revenue Sources

A business that depends heavily on one customer, product, or market is generally viewed as higher risk.

Diversification can improve buyer confidence by reducing revenue volatility.

Strategies include:

- Expanding into new geographic markets

- Launching complementary services

- Developing recurring revenue models

- Broadening your customer base

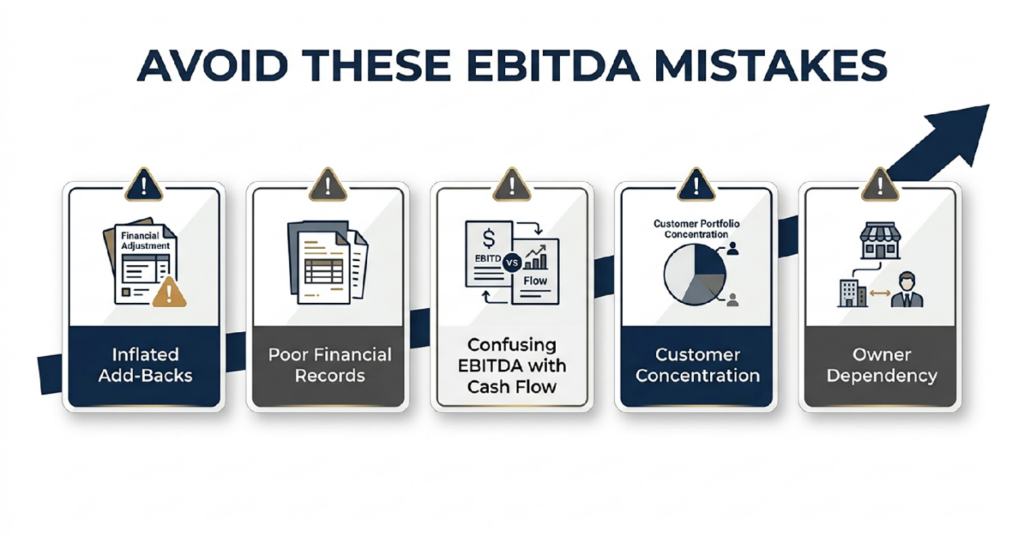

5. Reduce Customer Concentration

If a single customer accounts for a large percentage of revenue, buyers may discount the valuation due to perceived risk.

Building relationships with additional customers strengthens both earnings stability and negotiating leverage.

6. Strengthen Financial Reporting

Accurate financial records make due diligence smoother and inspire confidence.

Best practices include:

- Maintaining clean monthly financial statements

- Separating personal and business expenses

- Reconciling accounts regularly

- Documenting all significant transactions

- Preparing clear support for potential EBITDA adjustments

Transparent reporting reduces delays and increases credibility during buyer reviews.

7. Plan EBITDA Adjustments Early

One of the most overlooked opportunities is identifying legitimate add-backs well before launching a sale process.

Working with experienced M&A advisors and valuation professionals can help:

- Identify acceptable adjustments

- Gather supporting documentation

- Prepare for Quality of Earnings reviews

- Reduce buyer objections during due diligence

- Present a more accurate picture of sustainable earnings

Early preparation often leads to stronger negotiations and a smoother transaction.

Common EBITDA Mistakes Business Owners Make

Understanding EBITDA is one thing-using it correctly is another. During the sale process, even experienced business owners can make mistakes that reduce buyer confidence or lead to valuation disputes.

Here are some of the most common pitfalls to avoid.

1. Assuming EBITDA Is the Same as Cash Flow

Although EBITDA is often used as a proxy for operating cash flow, they are not the same.

EBITDA does not account for:

- Working capital requirements

- Capital expenditures (CapEx)

- Debt repayments

- Interest payments

- Taxes

A business with strong EBITDA can still experience cash flow challenges if it requires significant ongoing investment or has inefficient working capital management.

2. Inflating Seller Add-Backs

One of the quickest ways to lose buyer trust is by including aggressive or unsupported EBITDA adjustments.

Sophisticated buyers-and especially Quality of Earnings (QoE) providers-carefully review every proposed add-back. If an adjustment cannot be supported with documentation or is likely to continue after the acquisition, it may be rejected.

Overstating EBITDA can also prolong due diligence and weaken your negotiating position.

3. Focusing Only on Revenue Growth

Many business owners proudly highlight record sales, believing higher revenue automatically translates into a higher valuation.

However, buyers are more interested in profitable growth than revenue alone.

A company generating $20 million in annual sales with shrinking margins may be less attractive than a competitor producing $12 million in revenue with strong, consistent EBITDA.

4. Ignoring Working Capital

Even if EBITDA is strong, insufficient working capital can become a major negotiation point.

Buyers often evaluate inventory levels, accounts receivable, and accounts payable to determine whether the business has enough operating capital to continue running after closing.

Unexpected working capital adjustments can reduce the seller’s final proceeds.

5. Waiting Too Long to Prepare

Many owners don’t review their financial statements until after deciding to sell.

By then, opportunities to improve profitability, organize financial records, and document legitimate add-backs may already have been missed.

Preparing 12 to 24 months before going to market gives business owners significantly more flexibility to improve both EBITDA and buyer confidence.

Common Mistake

Don’t try to “manufacture” a higher EBITDA.

Professional buyers expect adjustments-but they also expect evidence. Unsupported add-backs, inconsistent bookkeeping, or overly optimistic assumptions often lead to lower valuations, longer negotiations, and increased scrutiny during due diligence. Credibility is one of the most valuable assets a seller brings to the table.

Frequently Asked Questions

1. Is EBITDA the same as profit?

No. EBITDA measures a company’s operating earnings before interest, taxes, depreciation, and amortization. Net profit includes all operating and non-operating expenses and reflects the company’s final accounting profit.

2. Why do buyers use EBITDA instead of net profit?

EBITDA removes financing decisions, tax strategies, and non-cash accounting expenses, allowing buyers to compare businesses more consistently and evaluate their underlying operating performance.

3. What is Adjusted EBITDA?

Adjusted EBITDA starts with reported EBITDA and removes unusual, non-recurring, or discretionary expenses-such as excess owner compensation or one-time legal costs-to better reflect operating performance.

4. What is Normalized EBITDA?

Normalized EBITDA represents the sustainable earnings a business is expected to generate under normal operating conditions. It is often the figure buyers rely on when determining business value.

5. What expenses can be added back to EBITDA?

Potential seller add-backs may include:

- Excess owner compensation

- Personal expenses paid by the business

- One-time legal settlements

- Relocation costs

- Non-recurring consulting fees

- One-time restructuring expenses

Every adjustment should be supported with clear documentation and may be subject to buyer review.

6. Is EBITDA used to value every business?

No. EBITDA is commonly used for established companies with consistent earnings, particularly in the lower middle market.

Smaller businesses may instead be valued using Seller’s Discretionary Earnings (SDE), while asset-intensive businesses, startups, or early-stage technology companies may require different valuation methods.

7. What is an EBITDA multiple?

An EBITDA multiple is a valuation metric that estimates a company’s Enterprise Value by multiplying Normalized EBITDA by an industry-appropriate multiple.

Enterprise Value = Normalized EBITDA × EBITDA Multiple

The appropriate multiple depends on factors such as industry, growth rate, recurring revenue, customer diversification, management depth, and overall business risk.

8. What is considered a good EBITDA margin?

A “good” EBITDA margin varies by industry.

Rather than comparing your business to a generic benchmark, buyers typically evaluate your margins against similar companies within the same industry and size range.

Consistently improving margins over time is generally viewed more favorably than a single year of unusually high profitability.

9. Who prepares EBITDA adjustments?

Business owners, accountants, valuation professionals, and experienced M&A advisors often work together to identify and document appropriate EBITDA adjustments before a business is taken to market.

During due diligence, buyers and Quality of Earnings providers independently review those adjustments.

10. Can improving EBITDA increase my business valuation?

Yes-but only when the improvements are sustainable.

Increasing recurring profitability, improving operational efficiency, and maintaining accurate financial records can strengthen buyer confidence and contribute to a higher valuation. However, valuation also depends on factors such as growth prospects, customer concentration, management strength, and overall business risk.

Final Thoughts: EBITDA Is Only the Beginning

EBITDA is one of the most influential metrics buyers use to evaluate a business, but it is only one part of the valuation equation.

Sophisticated buyers don’t simply apply a multiple to the EBITDA shown on your financial statements. They carefully analyze your earnings, identify appropriate adjustments, assess operational risks, and determine what your business is likely to earn under new ownership.

For business owners, this means that preparation matters just as much as performance.

By improving operational efficiency, maintaining accurate financial records, documenting legitimate add-backs, and planning well before a sale, you can present a stronger business to the market and improve buyer confidence throughout the transaction process.

At Horizon M&A, we help business owners understand how buyers evaluate companies, prepare for due diligence, and position their businesses for a successful exit.

Thinking about selling your business?

Contact Horizon M&A for a confidential business valuation and exit planning consultation. Our experienced advisors can help you understand your company’s true value, identify opportunities to maximize EBITDA, and navigate every stage of the sell-side M&A process with confidence.