Key Takeaways

- More than half of all small-business owners in the United States are over the age of 55, yet fewer than 20% have a formal, written exit plan.

- Manufacturing EBITDA multiples climbed from 10.2x to 11.1x between H1 2024 and H1 2025 — the market right now rewards prepared sellers.

- Companies that run their exit through an M&A advisory firm earn, on average, 31% more than those that go it alone.

- A well-prepared manufacturing business takes 11 to 18 months from advisor engagement to close.

- Customer concentration, owner dependency, and unreviewed financials are the three most common value-killers in manufacturing deals.

Introduction

You built a manufacturing business that actually works. Now you are thinking about what comes next — retirement, a liquidity event, or putting the business in the right hands. The problem is that selling a manufacturing business is nothing like selling a service firm.

Buyers scrutinize your equipment, your customer contracts, your workforce, and your margins in ways that catch unprepared owners off guard. Most manufacturing owners have done this once. The buyer sitting across from you has done it hundreds of times.

This manufacturing exit strategy playbook walks you through every stage: when to start, how your business gets valued, what buyers actually look for, and how to protect your number from LOI to close. If you are planning to exit in the next one to five years, this is where you start.

What Is a Manufacturing Exit Strategy?

A manufacturing exit strategy is a structured plan that a business owner executes to transfer ownership of their manufacturing company to a buyer, partner, or successor in a way that maximizes financial return, minimizes tax liability, and ensures operational continuity. Unlike an ad-hoc sale, a deliberate exit strategy begins 12 to 36 months before a transaction and addresses valuation, buyer targeting, deal structure, and post-close obligations. Owners who execute a planned process consistently achieve better outcomes than those who simply respond to unsolicited inbound interest.

This distinction is not theoretical. Research from First Page Sage found that manufacturing companies that ran their sale through an M&A advisory firm earned, on average, 31% more than companies that managed the process themselves.

The gap comes down to one factor: preparation. Buyers spend years learning how to acquire businesses. Most manufacturing owners do it once.

When Should a Manufacturing Owner Start Exit Planning?

The answer is almost certainly earlier than you think.

According to McKinsey’s 2026 analysis of the Great Ownership Transfer, more than half of all U.S. small-business owners are now over 55. Yet according to a 2025 Gallup Pathways to Wealth Survey cited in the same report, 27% of employer firms with owners aged 55 and older are either unsure of their long-term plan or intend to close the business permanently — destroying value they spent decades building. (Source: McKinsey Institute for Economic Mobility)

A separate analysis found that over 70% of Baby Boomer business owners expect to exit in the next decade, but fewer than 20% have a formal, written plan. That gap between intent and preparation is where value disappears.

The practical rule: if you want to close a deal in 2026 or 2027, your preparation window is already open. That preparation includes cleaning up financials, reducing customer concentration, documenting processes, and ensuring the business can operate without you in the room.

Signs you may already be late:

- Your top three customers represent more than 50% of revenue

- Your financials have not been reviewed or audited by an external CPA

- You are the primary relationship owner for key accounts and vendors

- Equipment maintenance records are incomplete or disorganized

- You have never obtained a formal, third-party business valuation

Horizon M&A Advisory Exit Readiness Assessment

How Is a Manufacturing Business Valued?

Manufacturing businesses are almost universally valued on an EBITDA multiple basis. EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization — the buyer’s proxy for normalized, recurring cash flow.

The multiple applied to your EBITDA depends on several factors: your niche and end market, customer diversification, growth trajectory, equipment condition, proprietary processes, and how operationally dependent the business is on you personally.

Current market data shows the following for private manufacturing companies:

| Business Profile | EBITDA Multiple Range |

| Small manufacturers, owner-dependent, <$2M EBITDA | 3.2x – 5.4x (median) |

| Mid-market, diversified customers, $2M–$5M EBITDA | 5x – 7x |

| Specialty/niche manufacturers with IP or proprietary process | 9x – 12x+ |

According to private transaction data aggregated by DHJJ, the EBITDA multiple for the manufacturing sector ranges from 3.2x at the 25th percentile to 10.4x at the 75th percentile, with a median of 5.4x across all deal sizes.

Importantly, the manufacturing M&A market is strengthening. Private sector manufacturing EBITDA multiples climbed from 10.2x to 11.1x between H1 2024 and H1 2025, driven by reshoring trends, supply chain diversification, and defense spending. (Source: First Page Sage, Manufacturing EBITDA & Valuation Multiples 2025 Report)

For middle-market deals overall, Capstone Partners reports that average M&A valuations settled at 9.8x EV/EBITDA in 2025, up from 9.4x in 2024 and 9.0x in 2023.

One important nuance: EBITDA ignores capital expenditure requirements. A 6x multiple on a capital-light specialty manufacturer is a fundamentally different asset than a 6x multiple on a manufacturer spending 15% of revenue on equipment. Buyers price CapEx intensity — and experienced sellers know how to frame it.

If your EBITDA is distorted by owner compensation, personal expenses run through the business, or one-time costs, a qualified M&A advisor will normalize those figures before going to market. Every dollar of legitimate add-back increases the valuation base.

What Do Buyers Actually Look for in a Manufacturing Acquisition?

Buyers are buying future cash flow. Everything they scrutinize ties back to one question: will this business generate predictable returns after I own it?

Here are the five factors buyers weight most heavily in manufacturing transactions.

1. Customer Concentration

If one customer represents more than 20–25% of revenue, buyers apply a risk discount or require escrow holdback provisions. Reducing concentration before going to market is one of the highest-ROI preparation moves a manufacturing owner can make.

2. Operational Transferability

Is the manufacturing process documented? Can a new owner step in without the founder’s institutional knowledge? Buyers pay a premium for businesses with written SOPs, trained supervisors, and equipment that does not require the founder to operate it. This is also called “management depth” — and it directly impacts your multiple.

3. Equipment Condition and CapEx Requirements

Buyers will commission a third-party equipment assessment during diligence. Deferred maintenance becomes a purchase price adjustment at the table, not a seller concession you can negotiate away. Address visible equipment issues before going to market, not during.

4. Workforce Stability

High turnover, key-person dependency, and unresolved labor dynamics all affect deal structure. According to BLS JOLTS data, manufacturing annual turnover runs 26–28% industry-wide. Buyers want a stable workforce that remains post-close. Documented retention practices and low turnover in key roles are quantifiable value-drivers.

5. Financial Quality

Audited or CPA-reviewed financials command higher multiples and generate fewer re-trade demands during diligence than compiled statements. If you are running on internal books with no external review, fix that 18 months before going to market. The cost of a quality-of-earnings engagement is trivial relative to what disorganized financials cost you at the negotiating table.

Already thinking about a sale? Horizon M&A Advisory works exclusively with manufacturing business owners and offers a confidential exit readiness assessment to identify exactly where your business stands today. Speak with a specialist at Horizon M&A

Horizon M&A Advisory Manufacturing M&A Services

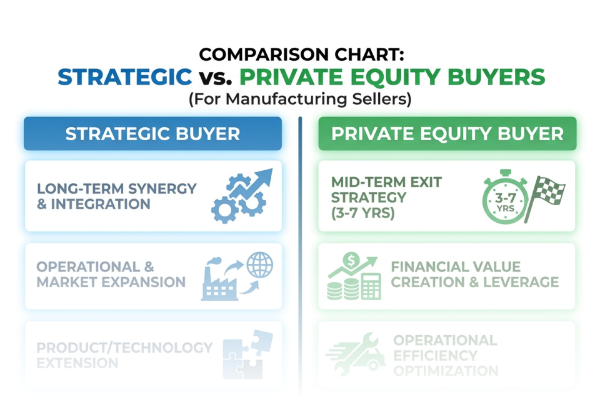

Strategic Buyers vs. Private Equity: Which Is Right for You?

This is one of the most consequential decisions in your exit. Most manufacturing owners do not think about it until they are already in a process — which is too late to use it strategically.

Strategic buyers are companies in your industry or an adjacent one. They acquire your business because it adds capabilities, customers, geography, or technology to their existing platform. Strategics often pay the highest headline prices because they can model synergies you cannot achieve alone.

In fact, data from R.L. Hulett shows that in H1 2025, strategic buyers paid a premium EV/EBITDA multiple of 14.7x, compared to 9.6x for private equity sponsors. (Source: Manufacturing M&A Statistics 2025–2026 aggregating R.L. Hulett data) That gap is synergy premium — and it is real.

Private equity sponsors are financial buyers who typically acquire a majority stake, retain management, and grow the business toward a second exit in 4–7 years. PE is the right path if you want liquidity now but want to stay involved, roll equity, and participate in a larger outcome later. Add-on acquisitions accounted for 58.2% of PE sponsor activity in 2025, meaning sponsors are actively building platforms in manufacturing.

The decision framework:

| Factor | Strategic Buyer | Private Equity |

| Headline price ceiling | Higher (synergy premium) | Moderate to high |

| Speed to close | Slower (integration planning required) | Typically faster |

| Your role post-close | Often reduced or eliminated | Usually retained |

| Equity rollover opportunity | Rare | Common (typical 10–30% rollover) |

| Cultural fit risk | High | Moderate |

| Second-bite upside | None | Significant if business grows |

Neither path is universally better. The right answer depends on what you want: maximum cash at close today, or maximum total economic outcome over 5–7 years. A qualified M&A advisor runs a process that puts both buyer types at the table and lets competitive tension — not the first caller — set your price.

The 5 Stages of a Structured Manufacturing Sale Process

Understanding the process eliminates the anxiety. Here is what a structured manufacturing sale looks like from engagement to close.

Stage 1: Exit Readiness Assessment (Months 1–3)

Identify gaps in financials, operations, and documentation. Normalize EBITDA, clean up books, and address any operational issues that will surface in diligence anyway. The goal: enter the market with a business that confirms what your CIM promises.

Stage 2: Preparation and Marketing Materials (Months 3–5)

Build the Confidential Information Memorandum (CIM), prepare a management presentation, create the initial qualified buyer list, and establish the data room. This stage is where the narrative around your business gets built — and narrative affects multiple.

Stage 3: Going to Market (Months 5–8)

Contact qualified buyers under NDA, collect Indications of Interest (IOIs), select finalists for management presentations, and begin gauging competitive tension among buyers.

Stage 4: LOI and Due Diligence (Months 8–14)

Negotiate the Letter of Intent, manage financial, legal, operational, and environmental diligence, finalize deal structure, and keep deal momentum from stalling. For lower-middle-market manufacturing deals, due diligence now averages 5.5 months. Preparation in Stage 1 directly compresses this timeline.

Stage 5: Closing (Months 14–18+)

Execute the purchase agreement, satisfy closing conditions, manage escrow provisions and rep-and-warranty insurance, transfer operational control, and close.

Total elapsed time for a well-prepared manufacturing business: 11 months from engagement to close is achievable; 14–18 months is typical. Unprepared businesses frequently take 24+ months or fail to close at all.

Common Mistakes That Kill Manufacturing Deals

These are the deal-killers that appear in diligence. Every one of them is preventable.

Mistake 1: Accepting the First Offer

The first inbound offer is rarely the best one. Running a competitive process with multiple buyers consistently produces higher valuations and better terms. Manufacturing owners who sell to the first strategic that calls them almost always leave money on the table — often 20–30% or more.

Mistake 2: Ignoring Environmental Liability

Manufacturing facilities carry environmental risk. Buyers commission Phase I and sometimes Phase II environmental site assessments. Undisclosed contamination is a deal-stopper. Know your exposure before the buyer does, and disclose proactively rather than reactively.

Mistake 3: Owner Dependency

If your business cannot function without you for two weeks, buyers will price that risk into the deal. The common outcome: a larger earnout component where you only receive the full purchase price if the business hits performance targets after you leave. Reduce key-person risk before going to market, not after.

Mistake 4: Undocumented Add-Backs

Add-backs require documentation. If you are normalizing for $200K in personal expenses or one-time costs, you need receipts, a clean narrative, and a QoE provider who has vetted the adjustments. Buyers and their quality-of-earnings advisors will verify every line item.

Mistake 5: No M&A Advisor

Manufacturing owners who self-represent in a sale process are structurally disadvantaged. The buyer’s team has completed hundreds of transactions. You have done this once. As noted earlier, unrepresented sellers in manufacturing earn an average of 31% less. The advisory fee — typically 3–8% of deal value — is recovered many times over.

FAQ: Manufacturing Exit Strategy

Q: How long does it take to sell a manufacturing business?

A well-prepared manufacturing business typically takes 11 to 18 months from initial engagement with an M&A advisor to final close. Due diligence for lower-middle-market manufacturing deals now averages 5.5 months on its own. The overall timeline extends when financial records are disorganized, when undisclosed liabilities surface during diligence, or when the owner has not addressed operational dependencies before going to market.

Q: What EBITDA multiple can I expect when selling my manufacturing business?

The EBITDA multiple for a private manufacturing business ranges from 3.2x at the low end to 10.4x at the high end, with a median of 5.4x across all deal sizes. Businesses with proprietary processes, recurring customer contracts, diversified revenue, and strong management teams command the upper range. Manufacturing multiples have been rising — climbing from 10.2x to 11.1x between H1 2024 and H1 2025 — making the current window one of the stronger seller markets in recent years.

Q: Should I hire an M&A advisor to sell my manufacturing business, or can I do it myself?

Hiring a qualified M&A advisor who specializes in manufacturing almost always results in a higher net outcome than self-representing. Advisors run competitive processes, understand buyer psychology, manage diligence, and protect deal terms through negotiation. Companies that used an M&A advisory firm in their sale earned an average of 31% more than those that did not. The fee is typically recovered in the additional value the process generates.

Q: What documents do I need to sell my manufacturing business?

At minimum, buyers require three years of financial statements (reviewed or audited), federal tax returns, a customer revenue breakdown, an equipment list with age and condition notes, real estate or lease documents, key employee agreements, environmental compliance records, and a description of manufacturing processes and certifications. Organizing these before going to market — not in response to buyer requests — is one of the most effective ways to shorten diligence and prevent re-trades.

Q: What is the difference between an asset sale and a stock sale for a manufacturing company?

In an asset sale, the buyer purchases specific assets and liabilities, leaving the legal entity with the seller. In a stock sale, the buyer acquires the entire legal entity including all historical liabilities. Buyers typically prefer asset sales because they limit liability exposure. Sellers often prefer stock sales for tax efficiency. The deal structure is negotiable and depends on deal-specific factors including the presence of environmental liability, existing contracts, and each party’s tax situation.

Q: How do I reduce customer concentration before selling my manufacturing business?

Reducing customer concentration requires 12–24 months of deliberate effort. This means actively developing new customer relationships, diversifying across end markets, converting existing customers to longer-term contracts where possible, and documenting that no single customer exceeds 20–25% of total revenue. This is one of the highest-ROI improvements a manufacturing owner can make before going to market — it directly expands the buyer universe and the valuation multiple.

Q: What is the “Great Ownership Transfer” and does it affect my manufacturing exit?

The Great Ownership Transfer refers to the wave of Baby Boomer business owners reaching retirement age. By 2035, roughly 6 million small and medium-size businesses will face ownership transitions, representing up to $5 trillion in enterprise value, according to McKinsey. Manufacturing is one of the most heavily impacted sectors. The practical implication for sellers: a growing supply of businesses coming to market means buyers will have more options. Differentiated preparation — clean financials, operational depth, and a structured sale process — is what separates deals that close at premium multiples from those that languish. (Source: McKinsey Institute for Economic Mobility)

Next Step: Work With a Manufacturing M&A Specialist

Selling a manufacturing business is a one-time event. You do not get a second attempt at the same outcome, and the mistakes that reduce your value are largely preventable with the right advisor by your side from the start.

Horizon M&A Advisory works exclusively with manufacturing business owners. We run structured, competitive sale processes that put multiple qualified buyers at the table, protect your terms through diligence, and close at the valuations we target.

If you are considering an exit in the next one to five years, the time to have this conversation is now — not when you are ready to sign.

Book a confidential manufacturing exit consultation at horizonmaa.com

There is no obligation. The conversation will tell you where your business stands today, what it is likely worth in the current market, and what specific steps need to happen before you go to market.

Horizon M&A Advisory specializes in manufacturing business exits. Learn more about our M&A process or contact us directly to start the conversation.